Apple stock surges as analysts forecast 45% upside potential

AAPL is at $272.83 in midday trading today, up almost 1%. This is over 10% higher than its recent trough at $246.63 on March 30. However, it could be worth considerably more.

Valuation and Upcoming Earnings

I discussed Apple's valuation in a recent article on April 7. I showed that AAPL could be worth $324.50, based on its forecast free cash flow (FCF) over the next 12 months.

That's still 19% over its price today, and implies there is good upside in AAPL stock.

Much will depend on its upcoming earnings results on April 30. For example, analysts now project revenue will be $466.44 billion this year ending Sept. 30, and $500.4 billion next fiscal year.

These forecasts show a next 12 months (NTM) revenue forecast of $483.42 billion. This is higher than those three weeks ago, as seen in my April 7 article.

Moreover, in its fiscal Q1 2026 ending Dec. 31, 2025, Apple generated $51.55 billion in free cash flow (FCF), representing 35.86% of its revenue, according to Stock Analysis. And, for the trailing 12 months (TTM), its FCF margin was 28.31%.

So, if Apple's fiscal Q2 results show that its FCF margin ranges between 28.31% and 35.86%, or 32% on average, the stock could be undervalued. Here's why.

Let's assume it generates a 30% FCF margin over the next 12 months (NTM):

0.30 x $483.42 billion NTM revenue = $145 billion FCF NTM

Using a 40x FCF multiple (i.e., a 2.5% FCF yield), that sets Apple's valuation at $5,800 billion, or $1.8 trillion higher than its $4.0 trillion today, as calculated by Yahoo! Finance. That implies a 45% upside in AAPL stock:

1.45 x $272.83 = $395.60 per share

Even using a lower 33.33x valuation metric (i.e., a 3.0% FCF yield), Apple would be worth $4,833 billion, or +20.8% over today's price:

1.208 x $272.83 = $329.58 price target

In other words, AAPL stock still looks undervalued, even after its recent runup. Moreover, analysts agree. Yahoo! Finance reports that the average PT from 47 analysts is $297.46. That's higher than the $295.32 PT seen in my April article.

Similarly, 28 analysts who have written recently about AAPL stock, as surveyed by AnaChart.com, have an average price target of $294.50.

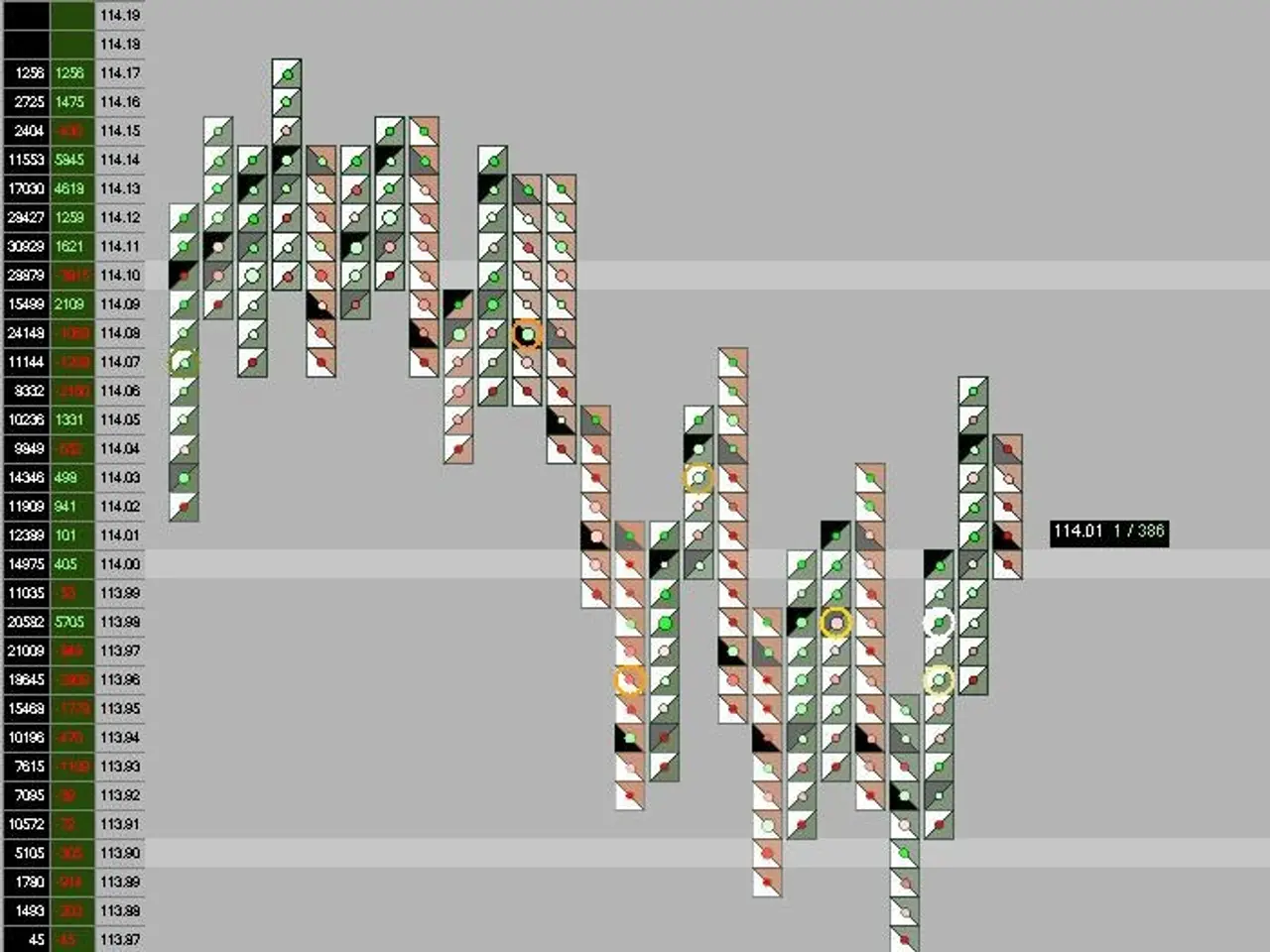

Unusual Put Option AAPL Activity

However, some investors believe AAPL stock may have risen too far, and/or its upcoming earnings will disappoint. That is why there is huge, unusual put option activity today.

This can be seen in today's Unusual Stock Options Activity Report.

It shows there are three tranches of unusual AAPL put options trading volume. These range from 27x to 42x the prior number of options outstanding at various strike prices.

The strike prices are at-the-money (ATM) or out-of-the-money (OTM), indicating that the investors who likely initiated these trades think AAPL will sink.

However, the sellers of the puts get to earn a good same-day or 2-day income, as well as a potentially lower buy-in breakeven point.

For example, the $275.00 put expiring today has a $2.58 premium, implying that the investor shorting these puts has a breakeven point of $272.42 (i.e., $275.00 - $2.58). That's slightly lower than today's price.

Moreover, the $272.50 puts expiring today and in two days have put premiums of $0.94 and $2.28, respectively. That sets their breakeven points (in case these are assigned) at

$272.50 - $0.94 = $271.56, with a 0.345% yield (i.e., $0.94/$272.50), and

$272.50 - $2.28 = $270.33 (i.e., -1% below today's price), with a 0.8367% yield (i.e., $2.28/$272.50).

The latter tranche is an attractive way for value investors to set a lower buy-in point (i.e., -1%) and get paid almost 1% over the next two days.

Given the potential upside in AAPL stock, as seen above, it may be an attractive way to play AAPL stock, despite its recent runup.

{kind=link}