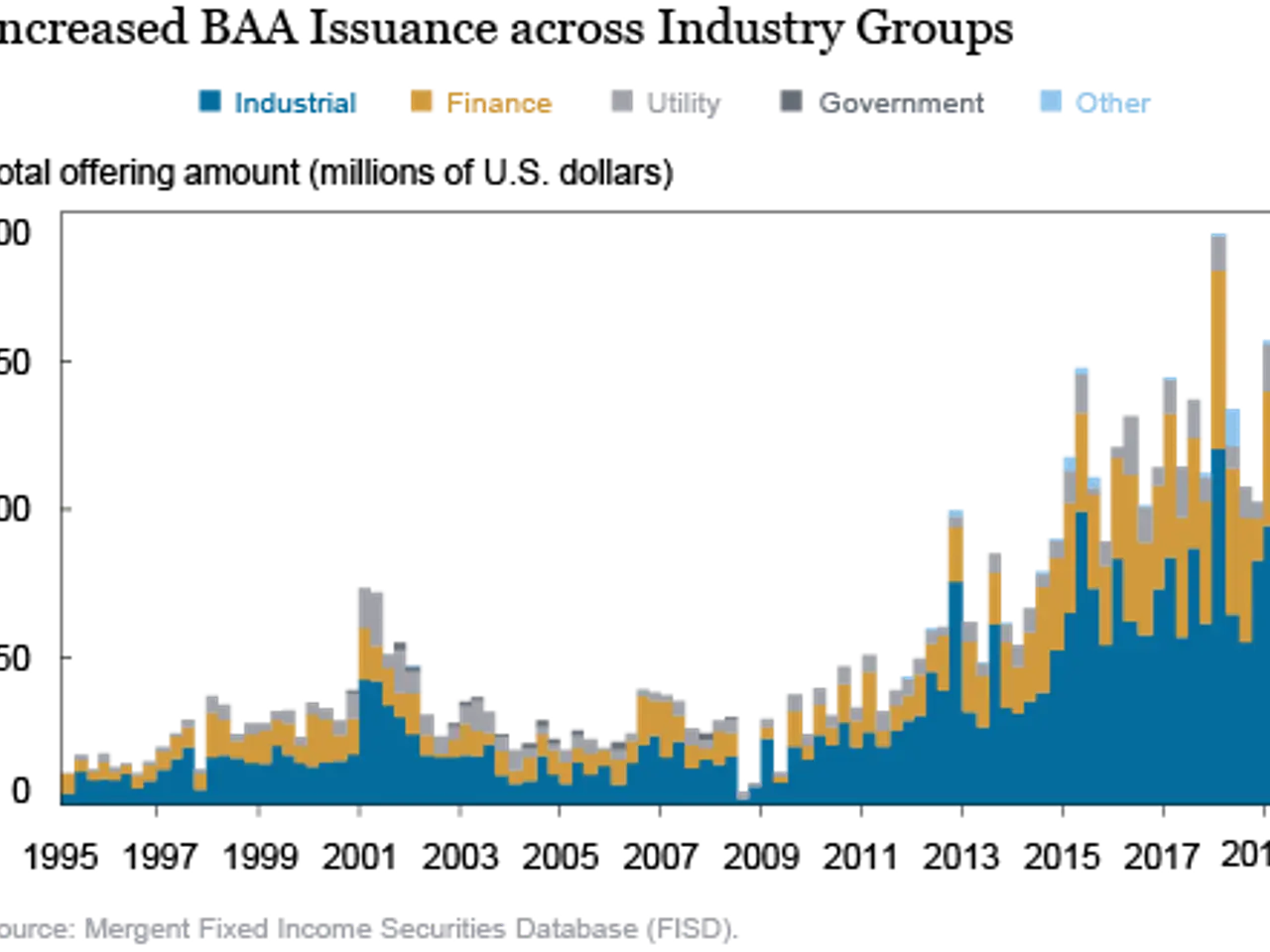

Quilter’s steady inflows clash with investor doubts in London’s finance scene

Quilter plc, a niche wealth manager listed on the London Stock Exchange, remains a topic of mixed discussion among investors. While its stock has struggled over the past year, recent updates highlight steady inflows and a push for greater efficiency. Yet, opinions on its long-term value remain divided.

The company’s share price has moved within a broad sideways range, finding support just below £1. Investors who purchased shares a year ago now face a near double-digit loss. This underperformance contrasts with larger, globally diversified finance companies, though Quilter’s valuation aligns with mid-sized UK financial services firms.

Financial media coverage has focused on two key areas: the firm’s strategic efficiency program and its consistent wealth management inflows. Despite these positives, analysts remain cautious. Most recommendations lean towards a 'Hold' rating, with only a few, like Berenberg, upgrading to a 'Buy' at a modest 215 pence target. The firm’s 2025 inflows appear solid, but volatility and strategic risks keep sentiment restrained. Long-term, income-focused investors see Quilter’s situation differently. The company offers attractive shareholder payouts, and its stable net inflows suggest resilience. However, without clear institutional backing, the stock’s future as either a value opportunity or a trap remains uncertain.

Quilter continues to balance steady inflows and efficiency efforts against market scepticism. While its valuation matches peers, the cautious analyst stance and modest price targets reflect lingering doubts. For now, the company’s ability to sustain payouts and inflows will likely shape its next moves.

{kind=link}